Sovereign Debt Markets Are Screaming. Is Anyone Listening?

The long end of the bond market is sending a signal that's hard to ignore. The US 30-year treasury just cleared 5% for the first time since 2007. Japan's 20-year bond hit its highest yield since 1997 as the government considers yet another supplementary budget to subsidize fuel costs ahead of summer. These aren't isolated moves. This is a global repricing of sovereign debt risk happening in real time. Bond markets across the developed world are telling you the same thing: governments have borrowed too much, for too long, and the bill is coming due.

Charlie Bilello put the US numbers in perspective: interest expense on public debt crossed $1.27 trillion over the last 12 months, another record. If it continues at this pace, it will surpass Social Security as the largest line item in the federal budget. Think about that. The US government will soon spend more money paying interest on past borrowing than it spends on the retirement safety net for 70 million Americans. And that's before the 5% yields on new issuance fully work their way through the debt stack. The doom loop is simple: higher rates mean higher interest expense, which means more borrowing, which means more supply, which pushes rates higher.

Look at this chart. The FRED data goes back to Q1 1947, when US interest expense on the debt was $5.35 billion. It took 73 years to 109x that number, reaching $586.4 billion in late 2019. Since then, it has more than doubled to $1.23 trillion in just six years. What took three quarters of a century to 109x took half a decade to double. The trajectory is parabolic, and it looks like a runaway train. As Lyn Alden likes to say, nothing stops this train. They are going to need to print. This is why Bitcoin exists.

Meanwhile, global money supply just crossed $121.9 trillion, up $17.1 trillion in two years, growing at 7-8% annually. The money supply chart speaks for itself. The trajectory is parabolic. Central banks are trapped between inflation that won't die and debt loads that require low rates to service. If the next Fed Chair Kevin Warsh comes in and cuts rates to ease the debt burden, he risks pouring gasoline on the inflation fire. If he holds or hikes, the interest expense spiral accelerates. There is no clean exit.

The inflation side of the trap is getting worse, not better. US electricity prices are up 50% in five years. PPI is leading CPI higher, with consumer prices already at their highest level in three years and producer data suggesting it's about to get much worse. The supply chain disruptions from the Strait of Hormuz standoff aren't going away. Data center construction just hit $50 billion annualized, up 437% since 2021, now exceeding office construction for the first time. That's a structural increase in electricity demand that hasn't even fully hit the grid yet.

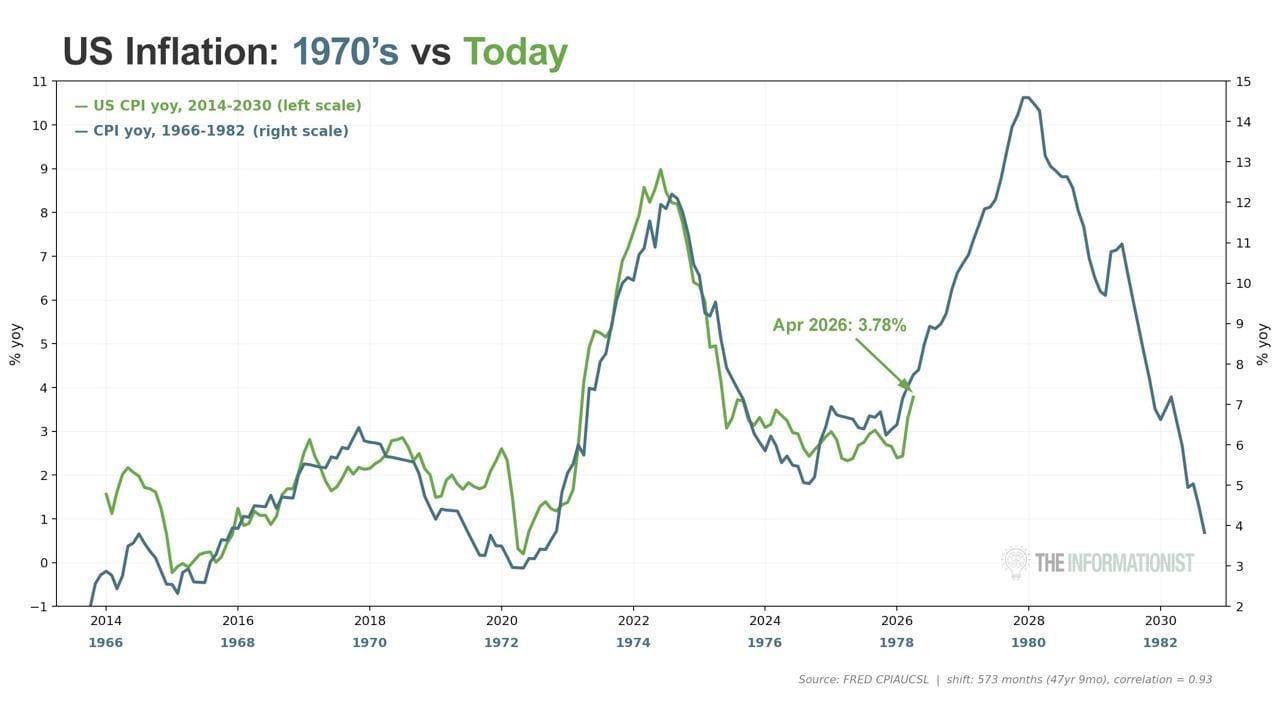

The Informationist's CPI overlay tells the story visually: current inflation tracks the 1970s pattern with a 0.93 correlation. April 2026 CPI sits at 3.78%, right at the inflection point where inflation re-accelerated in the late 1970s before peaking near 14%. The Fed declared victory prematurely then, too.

Jason Goepfert flagged something remarkable: the S&P 500 just set a record for the most components hitting new 52-week lows on a day the index poked above its prior all-time closing high. Ever. The six-week rally is the biggest since QE1, but performance is concentrated in a handful of stocks with AI and infrastructure exposure. The index is a mask. Underneath it, the average company is deteriorating while mega-caps absorb all the liquidity. This is what late-cycle concentration looks like.

The sovereign debt situation is deteriorating on multiple fronts. What makes this moment confounding is that there are genuine productivity gains from AI, and here in the United States there is an earnest re-industrialization campaign that should be good for the overall economy. But there is a growing dislocation between the haves and the have-nots, expressed through rising credit card delinquency rates, auto loan defaults, and consumer credit levels that suggest your average American is being squeezed while the top of the economy accelerates into the digital age.

We are trying to shed our skin and accelerate further into a digital, AI-driven economy. But we are carrying all this federal debt baggage with us, and it can only be resolved one of two ways: drastically cut spending, which DOGE proved is functionally impossible in the US political system, or debase the currency. Even though Kevin Warsh is posturing that he is willing to lower interest rates but does not want to expand the Fed's balance sheet, one has to wonder if his hand will be forced. Especially if a country like Japan loses control of its yield curve. Japan is the largest foreign holder of US Treasuries. If it has to sell those holdings to prevent its own bond market from running away and its currency from completely debasing, that will have direct effects on the US Treasury market.

All things to be aware of while Donald Trump and the administration sit down with Chinese officials to negotiate trade deals and a path forward. One has to wonder whether any of it matters if the sovereign debt crisis is accelerating underneath them. This is why Bitcoin exists. When you consider everything discussed here, yields, inflation, debt service, breadth collapse, and the impossibility of fiscal discipline, bitcoin is in bargain territory. Twenty-one million against all of it.

|