Galaxy Digital Converts $65M Bitcoin Mine Into $1B+ AI Revenue Machine

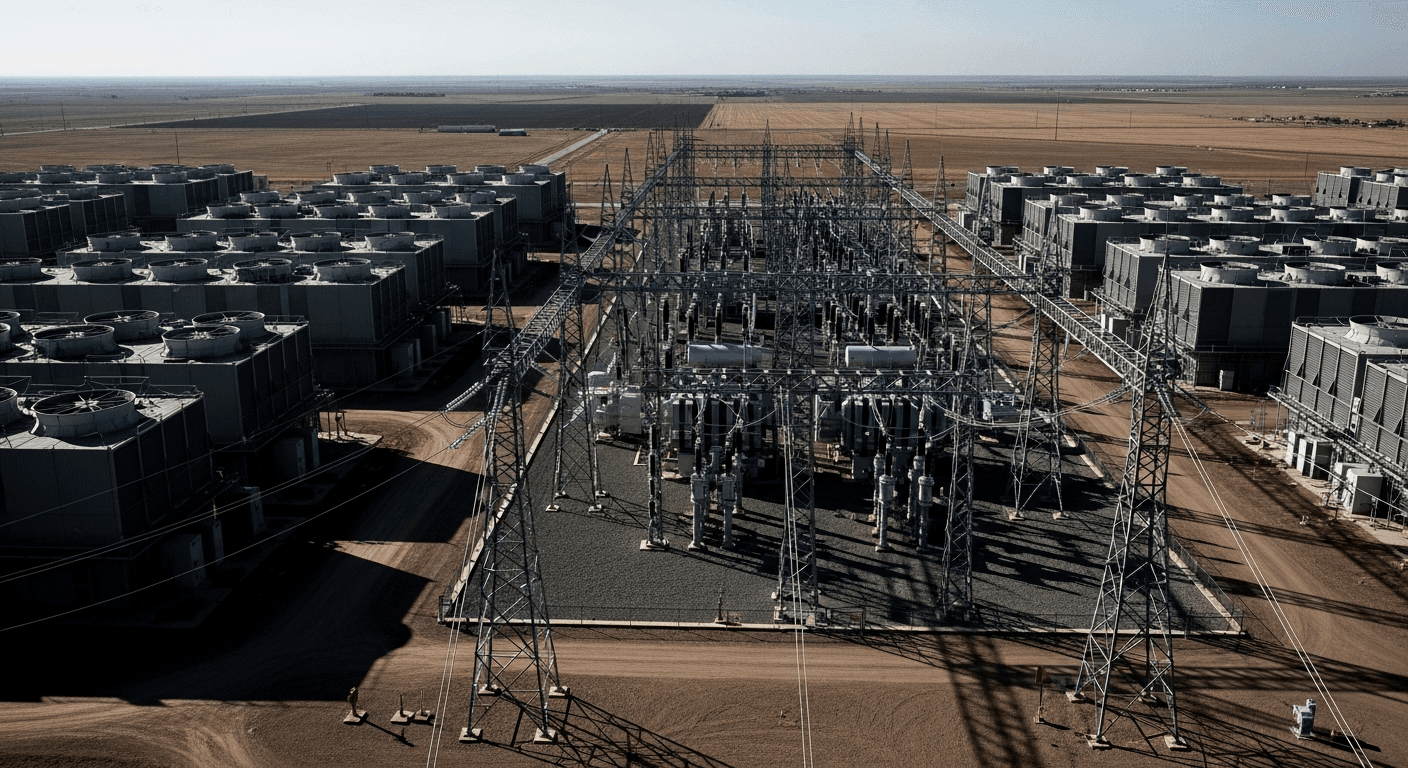

Galaxy Digital completed Phase I of its Helios data center campus on July 6, delivering 133 MW of critical IT load to CoreWeave under a 15-year lease. The former Bitcoin mining site, acquired from Argo Blockchain for $65M in late 2022, now anchors a $1B+ annual AI revenue stream.

Galaxy's Helios campus in West Texas just became the cleanest example yet of what post-halving mining economics actually look like for large-scale operators.

Key takeaways

- Galaxy Digital delivered 133 MW of critical IT load to CoreWeave at Helios on July 6, completing Phase I of a 526 MW, 15-year lease covering the full 800 MW of approved gross power at the site.

- The Dickens County campus was acquired from distressed Argo Blockchain for $65 million in December 2022. The full 526 MW buildout is projected to generate more than $1 billion in average annual revenue, with site-level EBITDA margins near 90% under a triple-net structure.

- With 830 MW of approved but uncontracted capacity remaining at Helios and Phase II deliveries targeted for H1 2027, Galaxy's pivot signals a structural reallocation of mining-grade energy infrastructure toward AI compute measured in decades.

Galaxy Digital announced on July 6 the completion of Phase I at its Helios data center campus in Dickens County, Texas, per the company's press release. The company delivered 133 megawatts of critical IT load to CoreWeave, with rent commencement beginning in Q2 2026. The site was purchased from Argo Blockchain in December 2022 for $65 million, when Argo hit financial trouble during the crypto winter and was forced to unload the asset.

The math from that point forward is worth sitting with. Three and a half years after closing a distressed deal on a Bitcoin mining site, Galaxy is now generating contracted AI infrastructure revenue on the same land under terms that post-halving mining simply cannot match.

What Galaxy Built and How It's Structured

Crews stripped out ASIC racks and replaced them with high-density electrical infrastructure built for GPU clusters. CoreWeave signed on as anchor tenant in March 2025 under a 15-year lease, then exercised additional options that brought its total commitment to 526 megawatts of critical IT load across three phases, per the $1.4 billion project financing facility press release. That covers the full 800 MW of currently approved gross power at Helios.

The lease is triple-net. CoreWeave brings its own GPUs and networking; Galaxy builds and operates the power and physical infrastructure, then passes through most operating costs. Galaxy projects site-level EBITDA margins near 90% on that structure. That is a company projection, not yet reported GAAP, but the structure itself makes the direction of the number self-evident.

Galaxy funded the buildout with a $1.4 billion project-level debt facility, approximately $350 million in equity, and a separate $460 million raise from an outside asset manager in October 2025, per the company's PRNewswire release. The full 526 MW buildout, once operational, is projected to generate more than $1 billion in average annual revenue, per the same press release.

Founder and CEO Mike Novogratz put it plainly in the announcement: "Helios is now generating revenue across its entire 133 MW of IT load, and greenfield work on Phase II is already underway. The demand for high-density, AI-ready power is not a cycle; it is a structural shift, and Galaxy is built to meet it."

The Miner-to-AI Arbitrage Is a One-Way Ratchet

The Helios deal is the sharpest data point yet on what the miner-to-AI transition actually looks like at institutional scale. Galaxy bought a distressed Argo asset for $65 million. The same land, same substation access, same power contracts now anchor more than a billion dollars a year in contracted AI revenue at margins that Bitcoin mining, at current hashprice, cannot get close to.

That gap is not closing anytime soon. The Stargate AI buildout and the broader wave of hyperscaler capex have repriced power for anyone who can deliver it at scale. AI tenants pay contracted, steady rates. Bitcoin mining revenue swings with hashprice. For an operator sitting on 800 MW of approved ERCOT capacity, the decision is not complicated.

The TFTC thesis here: the miner-to-AI arbitrage is a one-way ratchet as long as AI compute demand exceeds power supply and BTC block subsidies continue to halve. The trigger that reverses it is equally specific: if BTC price appreciation after the next halving is large enough to push hashprice sustainably above the per-MW equivalent revenue Galaxy earns under the CoreWeave lease, institutional operators rebuild mining capacity rather than lock it into decade-long AI leases. That is the scenario to watch. It requires a sustained hashprice recovery of a magnitude that the last two halvings did not produce.

The second-order effect for Bitcoin deserves attention. Every megawatt locked into a 15-year CoreWeave lease is unavailable to Bitcoin mining for a generation. Galaxy alone is talking about 526 MW committed. The broader pattern, visible across the sector, suggests the energy infrastructure that Bitcoin mining subsidized and built is being harvested by AI companies at scale. Smaller operators and vertically integrated ASIC manufacturers are left to carry an increasing share of hashrate. That sounds like decentralization. Whether it produces genuine decentralization or just a different concentration profile depends entirely on who fills the gap and where the next round of stranded power gets developed.

There is one more footnote worth noting. CoreWeave itself started as an Ethereum GPU mining operation before The Merge killed that business model. It pivoted to cloud GPU infrastructure and is now the anchor tenant in what was a Bitcoin mining site. Two proof-of-work-native companies are the principals in one of the larger AI infrastructure deals of 2026.

What Comes Next at Helios

Phase II, covering 260 MW of additional critical IT load, is already under construction. Civil and structural work is underway, with data hall deliveries expected in H1 2027. Galaxy controls more than 2,200 acres at the site. Approved capacity stands at 1.63 GW per a January 2026 SEC Form 8-K reflecting ERCOT approval, with potential to scale toward 3.6 GW pending further grid studies. Approximately 830 MW of that approved capacity remains uncontracted, leaving room for additional tenants or, theoretically, continued mining operations if the economics ever swing back.

The lesson for Bitcoin miners watching from the sidelines is not subtle. The moat was never the ASICs. It was the land and the power.

Sources

- Galaxy Digital PRNewswire, Phase I Completion, July 6, 2026

- Galaxy Digital PRNewswire, $1.4B Debt Facility Closure

- Galaxy Digital PRNewswire, $460M Strategic Investment, October 10, 2025

- Galaxy Digital SEC Form 8-K, ERCOT Approval, January 15, 2026

- Argo Blockchain press release, Helios sale to Galaxy, December 2022

Frequently Asked Questions

Not in any practical near-term scenario. The CoreWeave leases run 15 years with two five-year extension options. The physical conversion from ASIC racks to GPU-ready infrastructure, including new power distribution, cooling, and fiber, is not easily reversed. The exit from Bitcoin mining at Helios is effectively permanent for this generation of infrastructure.

Potentially, but not by design. As institutional-scale energy operators arbitrage their assets into AI leases, the remaining hashrate shifts toward smaller operators and ASIC manufacturers with vertically integrated power. Whether that produces genuine decentralization or a different concentration profile depends on who steps into the gap and at what cost of capital.

Power is zero-sum at the site level. A megawatt committed to CoreWeave under a triple-net lease cannot run ASICs at the same time. Galaxy's 830 MW of approved but uncontracted capacity at Helios leaves headroom where mining is theoretically possible, but at current hashprice, locking that capacity into an AI lease at projected 90% EBITDA margins is the easier capital allocation decision by a wide margin.