Bitcoin's network effects have profound effects on the companies building in the space.

I wrote about the bitcoin infrastructure flywheel several years ago. The premise was simple: investing in bitcoin infrastructure improves the network and makes it more valuable, which in turn creates increased demand and more users, thereby driving further investment and infrastructure buildout as the cycle continues. That is, investing in bitcoin technology drives network effects to the industry.

This has been a core part of Ten31’s thesis, and we have deployed over $125 million of equity into the bitcoin ecosystem over the last several years with this understanding. Our thesis still very much remains intact, and more investors over time will come to realize the merits of our strategy as bitcoin continues to eat the world. If understanding the flywheel from investing in bitcoin infrastructure is Bitcoin Technology Investing 101: Industry Network Effects, in this essay I would like to present the next level topic, Bitcoin Technology Investing 201: Portfolio Network Effects.

A Primer on Network Effects

Network effects is by now a common concept, popularized in the mid-90s by W. Brian Arthur with Increasing Returns and the New World of Business. Arthur pointed out that while traditionally there had been an assumption of diminishing returns in a market (that is, “products or companies that get ahead in a market eventually run into limitations, so that a predictable equilibrium of prices and market shares is reached”), he saw evidence that in the world of technology, information, and ideas, the mechanisms at play could drive increasing returns instead: that is, the tendency for that which is ahead to get further ahead; or, more practically, as a company or product with network effects becomes more successful and scales, it actually will command increasing returns and share over time.

Early examples of businesses that capitalized on network effects were Microsoft and IBM, and more recent examples include Airbnb, Amazon, Google, Meta, and Uber. David Sacks at Craft Ventures illustrated Uber’s network effects beautifully in 2014 when he tweeted “geographic density is the new network effect”. The network effects of Uber are obvious: the more drivers who sign up with Uber, the faster a customer can secure a ride; the faster a customer can find a driver, the more customers will want to sign up; and the more customers sign up, the more attractive Uber becomes to drivers.

While the graphic above is applied specifically with respect to geographic saturation, it is easy to apply the concept more generally to any business with a network effect, particularly so-called marketplace businesses like Uber which provide a technology platform to connect providers (sellers) on one end and users (buyers) on the other. As the marketplace grows, it becomes a better value proposition for both providers and users, and this results in a more valuable tech platform for its owners.

From Metcalfe’s law many will be aware the value of a network generally increases exponentially with scale, not linearly. As such, successfully investing in tech-enabled marketplaces with network effects has been a very lucrative business. Many investment firms have cemented their legacies based on the success of an early investment in just one of these marketplace businesses which later became dominant in its sector. However, marketplaces and network effect businesses can also present a number of potential issues and challenges for not just the participants on each side, but also the companies building the platforms and their investors:

Bitcoin Network Effects Powering an Investment Portfolio

One of the most underappreciated aspects of investing in the bitcoin ecosystem is the open and interoperable nature of the bitcoin protocol and the benefits that accrue to all participants from development in the space. Any developer, entrepreneur, or business can build on top of bitcoin’s standards and immediately plug into the scale of the network and both benefit from and contribute to its development over time.

What this means is that unlike what we’ve seen in the traditional Silicon Valley VC world, building and investing in exciting bitcoin technology companies is not zero sum. The success of one company does not have to be detrimental to another. This is because the network effect being developed is not at the company level, but actually at the industry level (i.e. across the entire bitcoin ecosystem).

At its core, money is the ultimate network effect. Money generally converges around one medium because its utility is liquidity, and liquidity consolidates around the most secure, long term store of value. Those who are contributing to bitcoin and building infrastructure interoperable with the bitcoin network are therefore enhancing bitcoin’s network effect as superior digital money and strengthening the ecosystem around it in which all participants operate. There are numerous benefits:

This last point is perhaps the least recognized aspect of the intra-bitcoin network effects and the point I want to emphasize the most. Because of the interoperability of bitcoin and its industry wide network effects, there are mutual benefits to collaboration and opportunities for partnership which are simply infeasible in traditional industry when competing standards, closed systems, and legacy competitive zero sum dynamics are often at play. Consider Venmo and Paypal: Venmo has been owned by Paypal for more than a decade, yet payments between the two are still not integrated. And that is within the same company; integration between separate companies will clearly present additional challenges.

The bitcoin network benefits from the opposite dynamic. Not only is interoperability ensured by compatibility with the base protocol, but the next order effect is an environment where collaboration can occur in interesting and unconventional ways, such as between companies which might otherwise be viewed as competitors in a traditional, non-bitcoin sense, or between seemingly unrelated companies whose only common ground is operating in the bitcoin network. One such example from within our portfolio is between Strike and Primal. Strike provides the backend bitcoin infrastructure which allows Primal to offer a native bitcoin wallet and bitcoin payments in-app within Primal’s broader social networking features. While there are many traditional companies that offer backend payments infrastructure for social media or online communities, the open source nature of bitcoin and nostr means Primal and Strike can still benefit from users within the network who are not locked into either business, and this is unprecedented. When viewed through a bitcoin lens, the aperture for collaboration presents compelling opportunities for groups to pursue shared objectives in an advantaged way relative to doing it alone.

At Ten31 we began seeing glimpses of this dynamic as our investment portfolio grew from 10 companies to 20 companies and beyond, and as the interconnectivity between these companies increased. Below is a depiction of the portfolio connectivity today as compared to two years ago. Each dot represents a specific company I have kept anonymous for purposes of this exercise, and each line indicates where there is a collaboration, official integration, or formal relationship in place between companies. No dots have moved positions from the left chart to the right; only new dots have been added (with new Ten31 investments over time), and new lines have been connected indicating increased collaboration across the group.

It will be easy for any reader to gloss over the above graphic and not appreciate how remarkable the level of connectivity is and the potentially significant implications that follow, so I urge you to pause and think about this. I draw a number of initial conclusions from this graphic:

The secret sauce to all of this of course is the bitcoin network effects. Everyone is rowing in the same direction. In addition, part of the portfolio effect is the ability of Ten31 to help facilitate connections between companies where a mutual relationship might not initially seem obvious to the parties involved, or where the Ten31 relationship can be additional common glue between companies to help reduce friction and encourage closer collaboration. As I have described previously, we created the Ten31 Tribe for exactly that reason–as a network of founders, investors, supporters, and interested parties whose main interest was actively supporting each other and the ecosystem as a whole. As one of the founders we are backing recently put it to me, “one of the best values we get from Ten31 is through involvement with the Ten31 Tribe”.

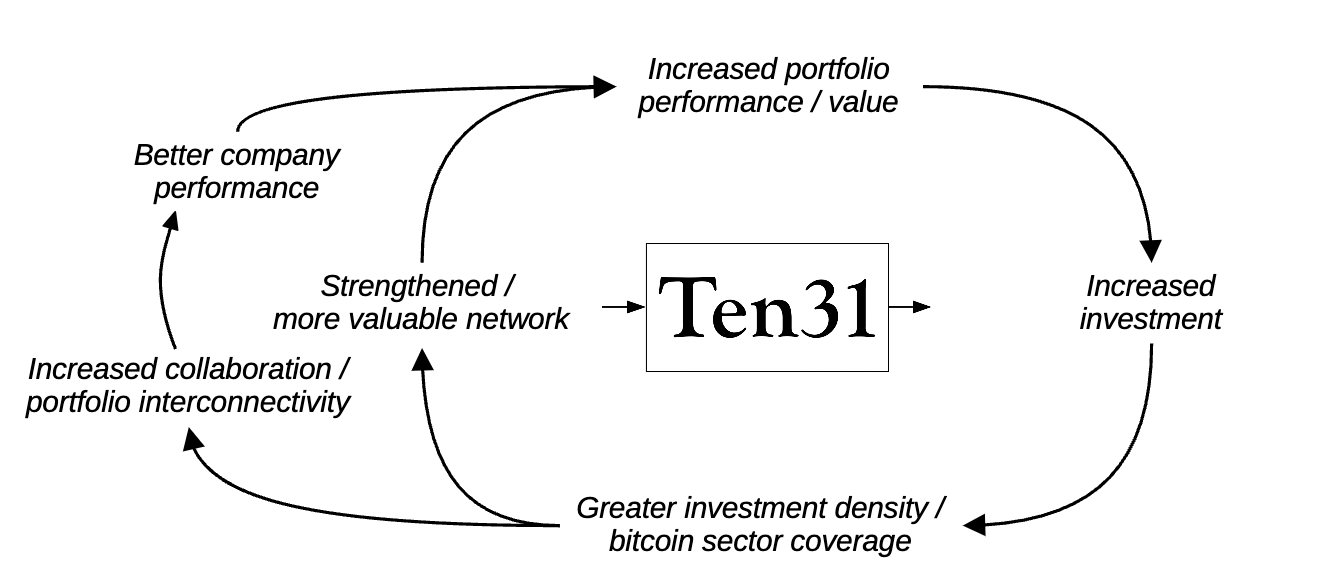

It is a profound idea that one company in a portfolio can drive value in an investment portfolio not just based on its own success, but can also contribute positively to the investment prospects of other investments in a portfolio. In this way the value of the portfolio can truly be greater than the sum of its parts by leveraging the interoperability and network effects of bitcoin. In other words, bitcoin technology is the new network effect. Increased bitcoin technology investment provides greater infrastructure density and strengthens the overall network, adding value to the network and portfolio; increased investment density increases the opportunities for collaboration, allowing for better company performance and increased portfolio value.

I also believe more favorable conditions persist with bitcoin’s industry and portfolio network effects as compared to the challenges I outlined initially with respect to business network effects:

Not many are paying attention yet, but I believe the next level of network effect economics is already at work in the bitcoin ecosystem. It is transforming the way companies work together and has significant implications. Bitcoin network effects are industry-wide and can deliver outsized value in a focused, interconnected investment portfolio. I am excited to see these concepts play out not just for the benefit of those companies in our portfolio and the investors supporting us, but also for the betterment of bitcoin as a whole as the network becomes more robust as a result.

This was originally published on Ten31's Insights blog. Find out more about Ten31 and our funds here.