An Investor's Case for the Biggest TAM on Earth.

In the few centuries since the inception of the joint-stock company, equity investors have developed a toolbox of intermittently useful frameworks and heuristics for evaluating potential investments. Some focus on valuation, guided by the mantra that there’s always a price at which any investment can become attractive. Others anchor to market leadership, arguing that more often than not, you’ll succeed just by backing the best of the best. But one theme that unites virtually all investors is the search for large total addressable markets (or “TAM”). Explicitly or implicitly underpinning all discussions of valuation, competitive analysis, and projected run-rate profitability is this basic question of TAM: at the end of the day, how big is the prize?

This obsession with TAM, especially prevalent among earlier-stage investors, stems from a simple expected value calculation any investor naturally has to make when deploying capital. For a given probability of success and holding all else equal, a larger addressable market translates to a greater revenue opportunity and a higher probability-adjusted return on investment. TAM is far from the only factor that explains investment returns, but it is a very powerful lever – it is almost always better to be a decent company in a fantastic market than a fantastic company in a middling market, as operational efficiency and defensible share will only get you so far if your market has reached its natural ceiling.

A few decades ago, internet-enabled software began, in the memorable phrasing of Marc Andreessen, “eating the world.” Said another way, its TAM exploded. Internet-enabled software’s addressable market became one of the largest of any industry because its dematerialization of previously physical products and services collapsed the marginal cost of information storage and transfer, opening up new ways of producing and consuming that would eventually impact every business and consumer in the world. This became the foundation for arguably the most successful investing theme of all time: riding the software wave up.

By now, this is a decidedly consensus view among investors, but what remains highly underappreciated by virtually all market participants is that we currently stand on the precipice of another even more disruptive theme: today, bitcoin is eating the world. Just as software and the internet dematerialized information and communication, bitcoin has dematerialized the most fundamental primitive of economic interaction – money itself – and consequently opened up step-function improvements and entirely new applications across industries. And since money is half of every transaction and commerce at virtually every scale is dependent on and downstream from it, bitcoin’s addressable user base will ultimately extend, like the internet before it, to every person on the planet.

As software ate the world, the greatest economic beneficiaries were the companies that carved out durable market positions as providers of software infrastructure and software-powered services, as well as the incumbents that moved first to adapt to this sea change. As bitcoin eats the world, the same will be true of innovative startups and forward-thinking blue chips that embrace bitcoin and leverage its unique capabilities. Internet-enabled software’s TAM is massive, but if bitcoin follows a similar adoption curve, then bitcoin infrastructure will become the biggest TAM on earth, and equity in the ecosystem’s bellwether companies will become the next generational investing theme. Crucially, though, few investors have yet to fully realize what’s about to happen – unlike in August 2011, when Marc Andreessen wrote his famous piece and many could already see the writing on the wall, this thesis is currently well outside consensus, meaning the asymmetric upside opportunity for those investing in bitcoin infrastructure today will be orders of magnitude greater.

We acknowledge this will sound like a bold claim to many investors, but we believe it is also set to become an increasingly consensus view over the next decade. If we’re right about bitcoin’s ultimate fate, the rest of our thesis at Ten31 falls neatly into place, as we’ll show below. So why do we believe bitcoin will eat the world?

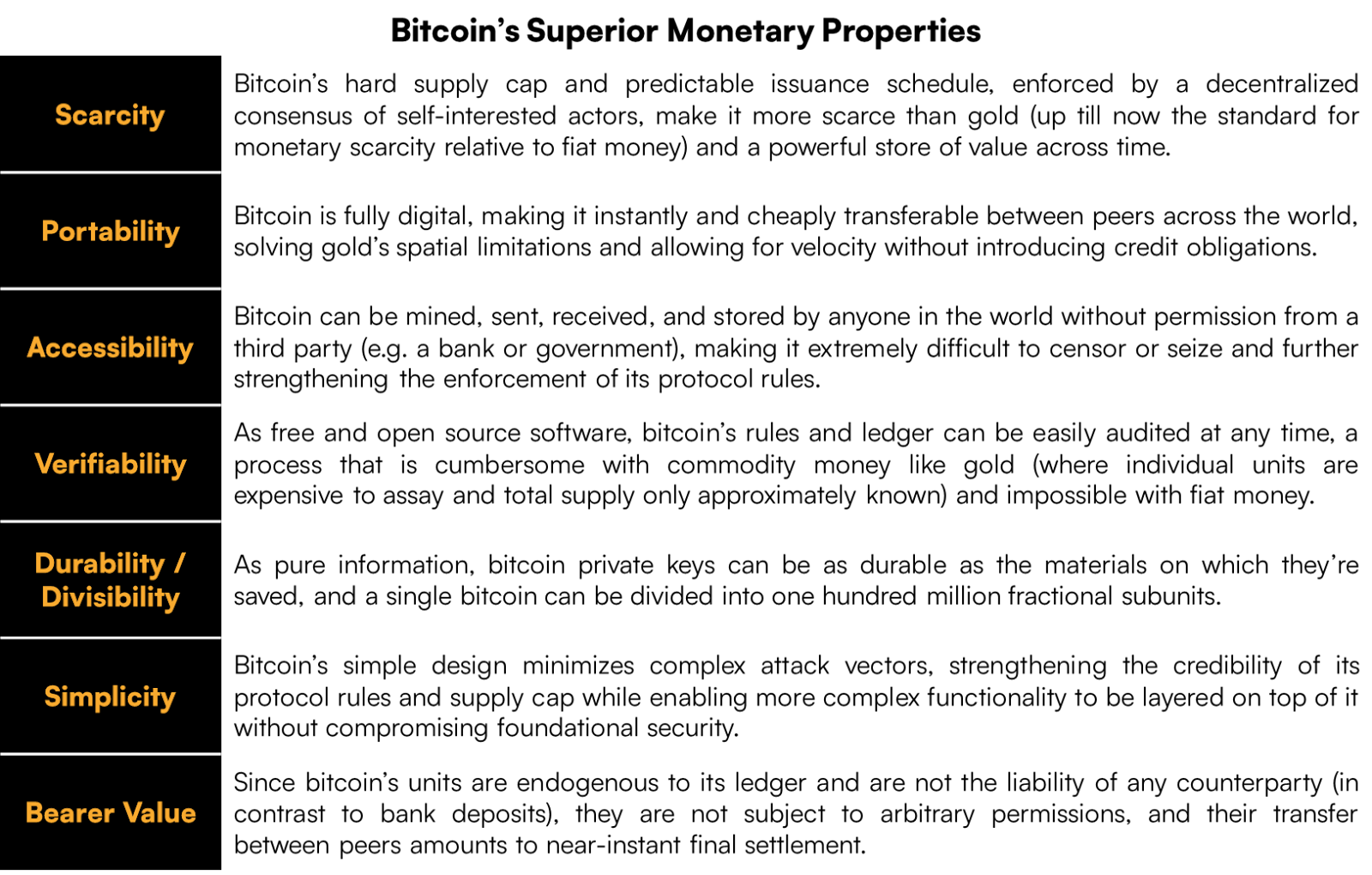

Most simply, bitcoin is superior monetary technology, and as knowledge of it distributes over time, there is no self-interested economic actor in the world that will be able to ignore it.

As (i) parabolically growing global debt necessitates accelerating debasement of even the most stable fiat currencies, (ii) price inflation across both essentials and durable assets marches higher, and (iii) more governments and banks around the world move to seize deposits and censor payments, the value of the properties above will become abundantly clear to billions (in most cases this will be an instinctive realization rather than an academic one). Even if these trends were all to reverse tomorrow, the superiority of bitcoin’s monetary properties would still tend to push its adoption forward, as economic actors will always prefer to store more rather than less wealth over time and will converge on using and saving in the currency that best facilitates that goal (at the expense of both fiat currencies and “altcoins” that fail to effectively compete with bitcoin as money).

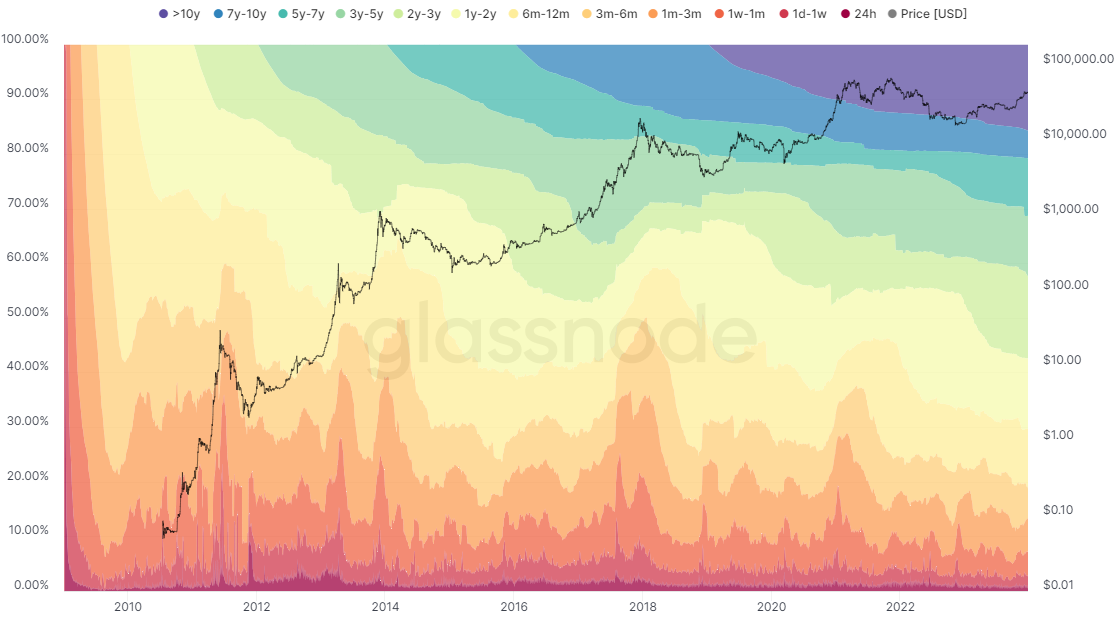

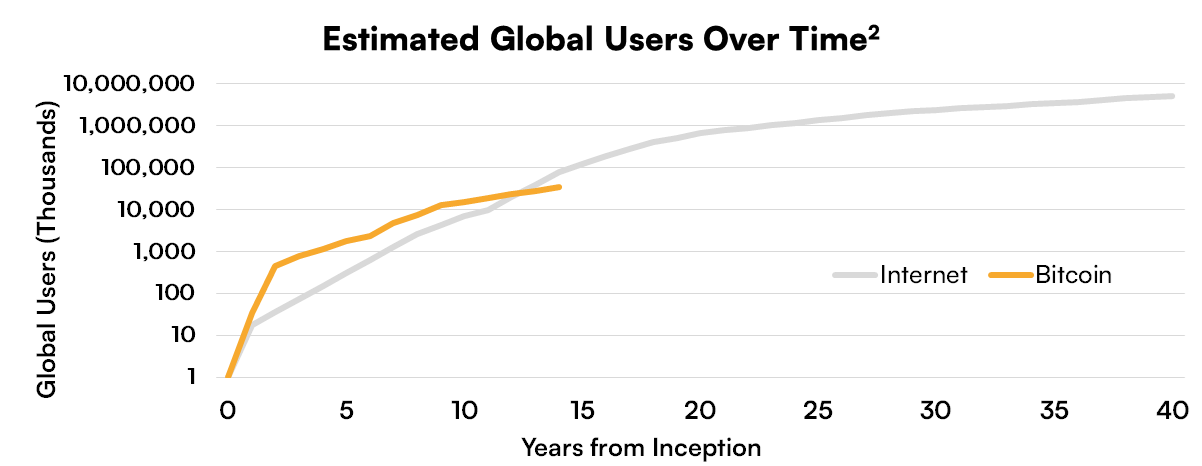

Fifteen years in, bitcoin has now withstood a barrage of stress tests that have both demonstrated and increased its resilience, an incomplete list of which includes: four 80%+ price drawdowns; massive exchange hacks, bankruptcies, and rugpulls; “bans” by large sovereigns like China; and contentious hard forks of its code. These stressors help illustrate bitcoin’s antifragility, and each shock it survives boosts confidence in the network and the likelihood that bitcoin will continue to survive, thus drawing in more users and further increasing resilience in a virtuous cycle (the “Lindy effect”). This phenomenon can be directly observed in bitcoin’s on-chain data through “HODL Waves,” which illustrate a consistently growing proportion of bitcoin buyers turning into long-term holders:

Like the internet, bitcoin has dematerialized a fundamental pillar of economic interaction – in this case, monetary bearer value itself – and the two technologies’ adoption curves look remarkably similar. But while the benefits of the internet’s early incarnations were more abstract, bitcoin comes with a powerful adoption incentive baked in: the opportunity for rapid and unmatched accrual of purchasing power over time (or more colloquially, “Number Go Up”). Early adopters will reap outsized and compounding rewards from this trend (i.e. a greater share of finite available bitcoin) at the expense of laggards, incentivizing a self-perpetuating rush to move first. Inherent in bitcoin’s design, then, is its own engine of adoption growth. The only winning move is to play.

A comprehensive case for bitcoin’s monetization is beyond the scope of our current focus, but we encourage interested readers to dive deeper in the suggested reading highlighted at the end of this piece. Suffice to say that the investment case for bitcoin’s continued adoption and monetization is highly compelling, and we therefore expect its ultimate user base to be virtually everyone in the world.

Bitcoin’s design makes a set of trade-offs that collectively enable the best monetary technology in history, but as with any emerging, paradigm-shifting technology, accessing and using it effectively are not always intuitive for newcomers. Anyone first coming to bitcoin, even if they’re constructive on its potential as a store of value or permissionless means of payment, likely confronts a series of questions right away: What exactly is this thing? How does it work? How can I get some? How do I store it safely and send it cost-effectively? What else could I do with it?

Bitcoin today is in a similar phase of its life cycle as the internet in the early 1990s, when the befuddled hosts of the Today Show famously asked “What is internet?” By that point, at least 10-20 million people were already using the internet, yet it remained a totally inscrutable tool to most mainstream observers. To take a bearish view on this technology because it was difficult for casual users would have been a terrible trade – the right question was just how long it would take for developers and innovative businesses to build approachable tooling and applications on top of the fundamental primitives of the internet protocol stack. That work would be carried out over the following decade with the proliferation of browsers (Netscape, Internet Explorer) built on easy, point and click graphical user interfaces (Windows, MacOS) offering access to applications and websites enabling previously inconceivable modes of interaction and commerce (Google, Amazon, Netflix, Facebook, thousands more). Less than 15 years after that Today Show clip, most Americans would have a miniature internet-enabled computer with them at all times.

If bitcoin’s superior monetary properties continue to drive its growing adoption along a curve that looks roughly like the internet’s, then demand for acquiring, securing, and using bitcoin will naturally support demand for tooling, applications, and infrastructure to make all of that easy and practical for consumers and enterprises. This opens up significant opportunities for innovators to build businesses catering to this demand, with early movers like the companies in the Ten31 portfolio set to reap outsized rewards as they amass reputation, brand power, and network effects. In essence, this is the classic “picks and shovels” play, whereby investment in the enabling technologies supporting a major secular shift can provide levered returns on the underlying theme, like selling equipment to gold miners during a gold rush, oilfield services businesses that enabled the early days of oil and gas extraction, or modern tech titans that built the user-friendly tools anyone reading this takes for granted today.

Moreover, just as with software, the addressable verticals available to bitcoin infrastructure investors will also proliferate and compound as adoption grows and the application ecosystem becomes more sophisticated. Use cases and business models that are inconceivable today will become multi-billion dollar opportunities in short order in the same way that cloud computing – which depended on prior advancements in server architecture, network connectivity, and more – went from a ~$10 billion market to a half-trillion dollar revenue category over the past decade. Similarly, businesses like ServiceNow, Salesforce, and Shopify (all worth more than $100 billion) didn’t even exist at the turn of the century and couldn’t have gotten off the ground without work done by earlier innovators.

We’re already seeing many examples of these dynamics within the nascent bitcoin infrastructure market and in our own portfolio. Products like Strike’s Global Wallet, Coinkite’s Tapsigner, and Fedimint applications being built by Fedi and Mutiny are making bitcoin and the lightning network intuitive and accessible for billions of consumers, often in ways that require little direct interaction with bitcoin. Similarly, Unchained’s collaborative custody network and AnchorWatch’s bitcoin insurance platform bypass the technical burdens and black-box counterparty risks that have plagued bitcoin custody for much of its short history, laying the foundation for widespread institutional and enterprise adoption of bitcoin as a treasury asset. Few of these applications were on anyone’s radar as commercial use cases even five years ago, but the outlines of the value they will generate over the next decade are already coming into view.

Back in 2011, Marc Andreessen noted that internet-enabled software was taking off partially because “all the technology finally work[ed]” and could be “widely delivered at global scale.” We’re not quite there yet with all of bitcoin’s enabling technology, but the products above are clear evidence we’re getting much closer, and the companies building the infrastructure to make that a reality are in position to become behemoths. The first-order opportunity of this theme alone is likely in the trillions as bitcoin adoption advances parabolically upward, carrying bitcoin-native technology companies with it.

The “picks and shovels” thesis will prove to be a rich investing theme by itself, but it’s only the tip of the iceberg. Money is half of every transaction, so if bitcoin adoption proceeds as we expect, it will eventually touch virtually all economic activity in the world directly or indirectly. This tectonic shift in monetary technology is a trend that no commercial entity will be able to ignore indefinitely. Just as every company effectively had to become an “internet company” over the past few decades to both leverage the new capabilities offered by internet-enabled software and to keep pace with upstart competitors doing the same, so too will every business have to become a “bitcoin company” in some way to remain relevant. This will drive trillions of dollars of disruption to existing business models and open up massive new surface area for forward-thinking investors in bitcoin infrastructure.

The most obvious industries that will need to adapt include:

The second-order implications for industries well outside the sphere of payments and finance are just as substantial, and the effects are already becoming evident in markets as diverse as:

And even these verticals are still just scratching the surface. As we’ve addressed extensively elsewhere, the rapidly growing ecosystem of generative artificial intelligence technologies will converge with bitcoin and lightning in the near future thanks to bitcoin’s digitally native instant settlement assurances and high divisibility, which differentiate it from both fiat and altcoins and make it the ideal way to pay for AI compute resources. The last year has shown many early examples of that convergence, including the release of the L402 toolkit to help developers unlock the unique properties of lightning payments for AI applications, as well as the emergence of Nostr Data Vending Machines, a technique using lightning and nostr to outsource data processing requests to competing AI agents. Companies already expressing this theme in the Ten31 portfolio include StatMuse, which pioneered the use of Natural Language Processing (NLP) for sports data search and and has recently launched extensive bitcoin and finance data as its next search vertical, and Stakwork, which has been combining AI training workflows with instantly-settled lightning payments for several years. As the internet-native money of the future, bitcoin will be instrumental in powering the machine-payable web and the emerging economy of autonomous agents – if you’re bullish on AI, you should be just as bullish on bitcoin infrastructure.

The key intuition uniting all of these examples is that providing instant settlement of borderless bearer value is a unique and unprecedented phenomenon with derivative implications for every industry, and it will inexorably pull businesses that currently have nothing to do with bitcoin into bitcoin’s orbit. And as all these examples illustrate, this is not just speculation — we are watching it play out in real time across our portfolio. Bitcoin’s influence on a growing list of industries will lead to acquisitions of today’s foremost bitcoin companies, in addition to expanded addressable markets for bitcoin infrastructure investors as regular companies integrate bitcoin around the edges in their legacy businesses. To paraphrase Andreessen again: companies in every industry need to assume that a bitcoin revolution is coming.

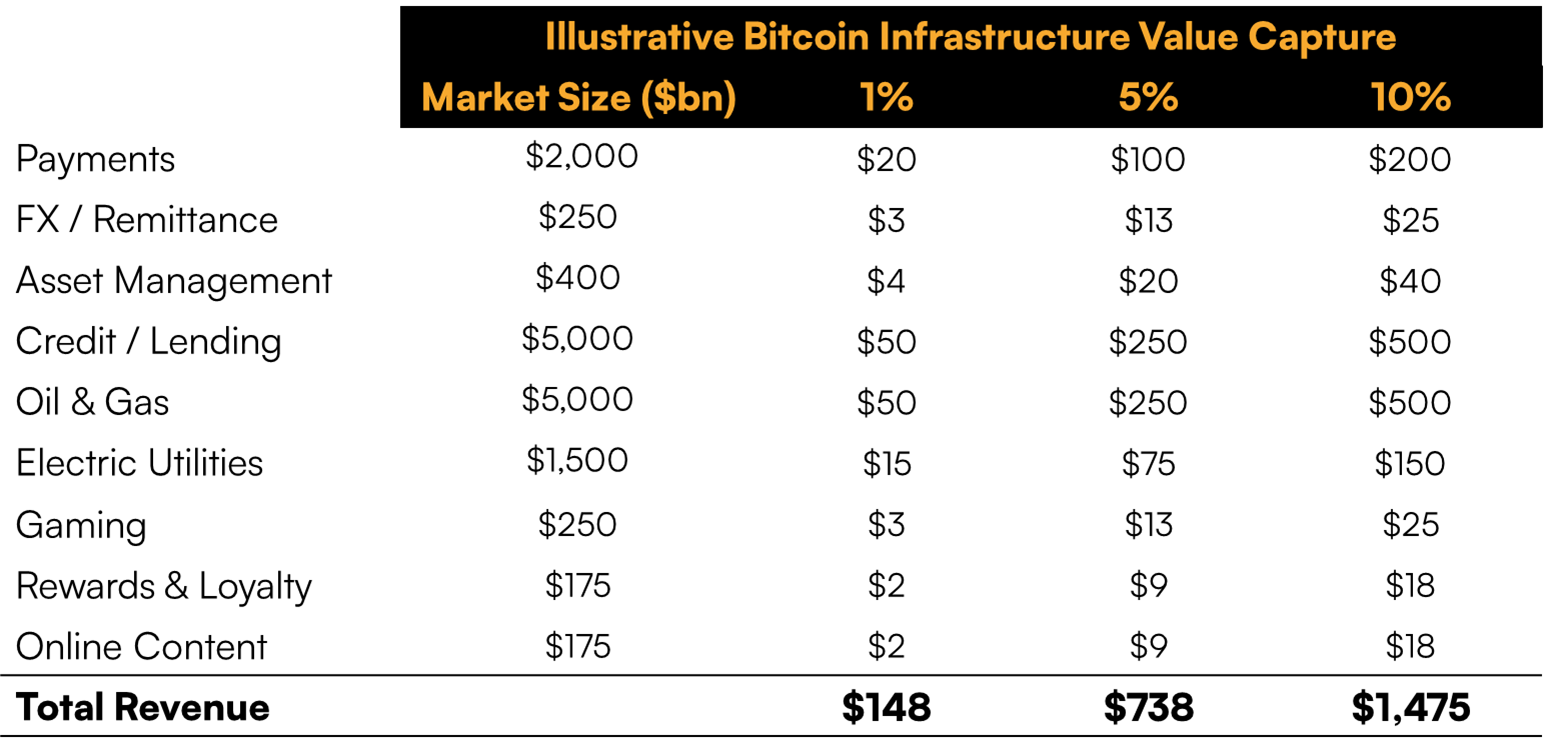

What might this bitcoin revolution look like in practice for the companies pushing it forward? As a very rough, incomplete guidepost for the kind of value capture this secular shift could generate, it might be instructive to look at the revenue generated by all the industries discussed above. If bitcoin infrastructure captures even 1% of the annual revenue of those massive industries, whether through establishing a place in their value chains or outright displacing legacy business models, it will be well on its way to becoming one of the biggest categories in the world.

Unlike any of these individual industries, bitcoin companies can capture a cross-section of all these disparate verticals thanks to monetary technology’s universal influence on all commerce. Even if bitcoin infrastructure captures only a minimal fraction of its most immediately addressable revenue pools – putting aside longer-term revenue opportunities like AI or telecommunications – it would still rival the size of the ~$200 billion SaaS market. Meanwhile, there’s a compelling case that bitcoin infrastructure should capture quite a bit more value in many of these categories, particularly those related to financial services.

But even that still only tells part of the story. Crucially, most of the applications we’ve discussed in this piece were fundamentally impossible before the advent of instantly settled, highly divisible, globally liquid, digitally native bearer money. This means that bitcoin infrastructure won’t just capture some portion of the existing pools of value discussed here, but also – like the internet before it – create totally new ones, which in turn means that despite the massive opportunity already at hand, many of the largest “bitcoin industries” of the future have yet to emerge. We might compare this dynamic to Netflix’s displacement of Blockbuster, which didn’t just siphon off the incumbent’s revenue base but dramatically expanded it through technology that was previously unavailable, or to the launch of the iPhone, which not only kicked off parabolic growth in the smartphone market but also laid the foundation for the more than $1 trillion of revenue built on previously nonexistent mobile app stores.

Taken together, bitcoin’s “picks and shovel” opportunities, its inevitable permeation into virtually all existing businesses, and the totally new industries its unique properties can enable will make bitcoin infrastructure the biggest TAM on earth over the coming decades. To return to the framework established earlier, this means equity investors focused on bitcoin infrastructure benefit from a massive advantage that should drive superior risk-adjusted returns – the prize is simply bigger here than anywhere else.

Finally and importantly for any investor evaluating these claims: the market still has yet to fully appreciate the implications of this thesis. Given that only a few hundred million dollars have been deployed into companies focused on bitcoin, whereas well over $25 billion have been channeled to the broader “crypto” ecosystem, it is safe to say virtually every capital allocator around the world is substantially underweight bitcoin infrastructure. Those that recognize the opportunity now will not only have access to some of the most compelling investments of the coming decade, but will compound their returns by front-running the flood of capital that will eventually arrive as this theme becomes more obvious. Even if there’s only a 1% chance our view is correct, the potential asymmetric upside of moving first is too great for any responsible capital allocator to ignore. At Ten31, we have already deployed over $100 million into this thesis, and we are just getting started.

To quote Andreessen one last time: That’s the big opportunity. I know where I’m putting my money.

Suggested Further Reading

Learn more about Ten31, our investment thesis, portfolio companies, and funds by visiting our website.