Time is an essential aspect of economics, often overlooked in conventional discussions. Julian Simon, a notable economist, emphasized that time is the ultimate resource. All human action and economic decisions occur across time, and production requires time as a fundamental input.

Economics is a social science that studies the production, distribution, and consumption of goods and services. It focuses on how individuals, businesses, governments, and nations make choices about allocating resources to satisfy their needs and wants. One of the fundamental concepts in economics is scarcity, which refers to the limited nature of society's resources.

Time is an essential aspect of economics, often overlooked in conventional discussions. Julian Simon, a notable economist, emphasized that time is the ultimate resource. All human action and economic decisions occur across time, and production requires time as a fundamental input.

Humans are mortal, meaning our time is inherently scarce. This scarcity makes time an economic good, as it is both valuable and limited. Unlike other goods, time is irreversible; we cannot buy back lost time or extend it indefinitely. The scarcity of time is what gives rise to all other economic scarcities.

Economic scarcity is a manifestation of the scarcity of human time. The economic problem can thus be reframed as the problem of economizing time efficiently. Because our time to produce goods is limited, all goods are scarce, regardless of their abundance on Earth.

Staff

Staff

The concept of "proven reserves" refers to the quantity of a resource that has been discovered and is extractable under current economic conditions. Simon's analysis of data from 1950 to 1990 reveals that the reserves for many commodities, such as lead, zinc, copper, and oil, have increased significantly despite higher consumption rates.

The idea that Earth's finite resources will run out due to human consumption is based on the misconception that proven reserves represent the total amount available. In reality, Earth is abundant with resources, and human innovation continues to uncover more. The true constraint is the time required to make these resources usable.

The scarcity of time introduces the concept of opportunity cost, which is the cost of forgoing the next best alternative when making an economic decision. Every action consumes time, and with time being finite, there is always another potential use for it.

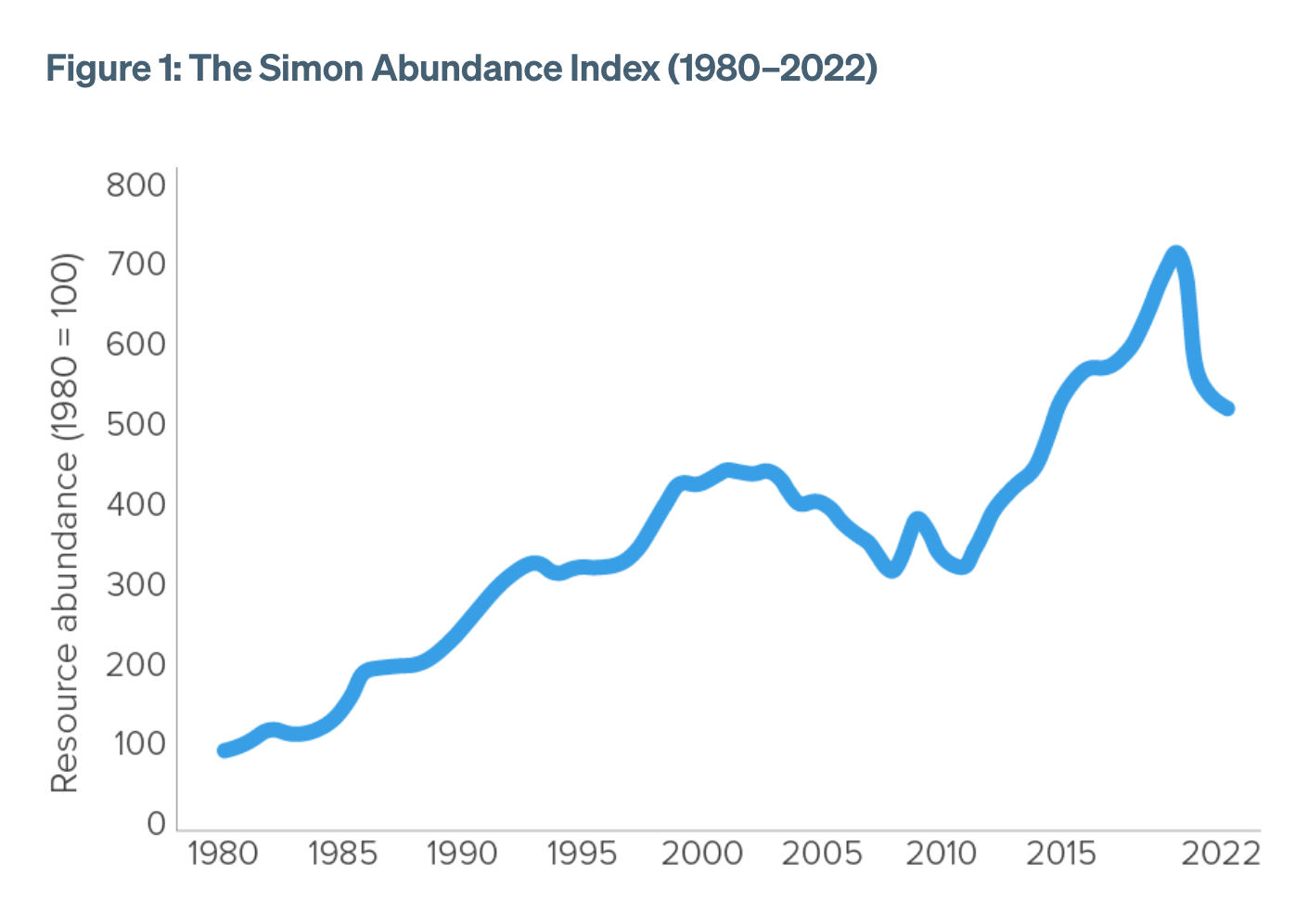

Developed by economists Marian Tupy and Gale Pooley, the Simon Abundance Index measures the price of commodities relative to human wages. Over 40 years, the index shows a 75% decrease in the time price of 50 basic commodities, despite a 75% increase in the human population.

Julian Simon famously bet with environmentalist Paul Ehrlich that the prices of selected commodities would decrease over ten years. Simon's victory demonstrated that resources become more abundant as humans find innovative ways to discover and utilize them.

Time preference refers to the universal human tendency to prefer present goods over future goods. It stems from the scarcity of time and the uncertainty of the future. This concept is central to understanding how individuals economize their time between labor and leisure, and how they trade present utility for future benefits.

The analysis of economic scarcity through the lens of time provides a nuanced understanding of resource allocation. By recognizing time as the ultimate resource, we can better comprehend the dynamics of production, consumption, and the continuous expansion of proven reserves, which challenge the notion of finite resource depletion.